State of the American Debt Slaves: Fed “Confounded” as They Pay Down Credit

Forbearance Effect: Serious delinquencies of mortgages & student loans plunge to record lows as delinquent loans in forbearance don’t count as delinquent.

By Wolf Richter for WOLF STREET.

Our always amazing American debt slaves are still borrowing, mind you, but to the great consternation of the Fed, they’re reducing their debt where banks and shadow banks make a big pile of their money: credit cards and other high-interest-rate debt such as personal lines of credit.

Total household debt – mortgages, HELOCs, credit cards, auto loans, student loans, and other debt – rose by $85 billion in Q1, to $14.6 trillion, according to the New York Fed’s Household Debt and Credit report Wednesday afternoon, based on data from Equifax.

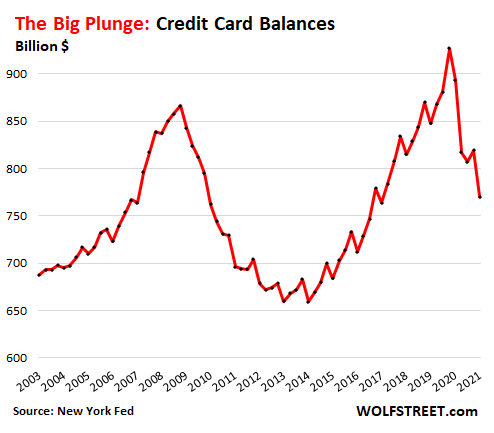

But the thing is, Americans paid down their credit cards in Q1 by the second largest amount ever, by $49 billion, behind only the $76 billion they paid down in Q2 2020. “One of the most confounding changes in debt balances,” the New York Fed called it in a blog post. In the five quarters since Q4 2019, the last full quarter of the Good Times, Americans have paid down their credit cards by $157 billion.

In the wake of the Financial Crisis, credit card balances also plunged, but they took a lot more time – four years, from Q4 2008 to Q4 2012 – and it wasn’t because consumers paid them down, but because consumers defaulted on them, and those balances were written off.

This time around, there are waves of stimulus money, and PPP loans, and extra unemployment benefits, and eviction bans, and foreclosure moratoriums, and rent aid, and whatnot. The government has taken a fire hose and has sprayed the land with cash, and it has put collection of some debts on hold.

Many consumers received the series of stimmies, starting in April 2020. For many of them, it was extra money that suddenly showed up, and instead of putting it into a checking account where it serves no purpose, some people used it to pay down their usurious-interest rate debt – smart thing to do.

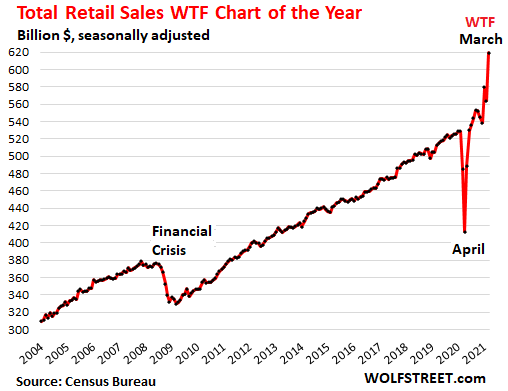

Some of the stimmies were also spent on goods, as retail sales have experienced a glorious previously unheard-of WTF spike despite the drop in credit card balances:

Those people who used their stimmies to pay down their credit cards and those that used their stimmies to contribute to the WTF spike in retail sales may have been two separate groups of people with only partial overlap.

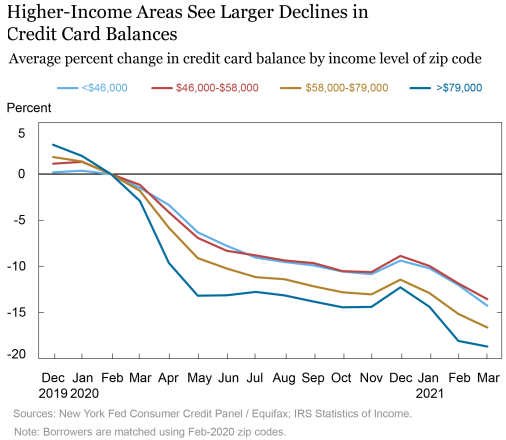

People living in higher-income zip codes paid down their credit cards more than people living in lower income zip codes, the New York Fed found, based on data from the IRS on income levels by zip codes, and Equifax data on credit card balances for those zip codes.

In high-income zip codes (over $79,000), average credit card balances have fallen by 19% over the year; in the lowest-income zip codes (below $46,000), average credit card balances have fallen by 15%:

The fact that the Fed is trying to sort out this phenomenon of Americans actually paying down their usurious-interest debts and depriving the banks of some serious moolah shows how serious this situation is.

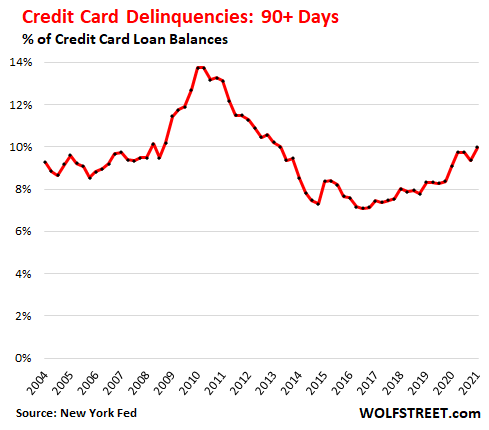

Despite the stimmies and the other government moneys washing over consumers, the serious delinquency rate (90+ days past due) has been high and in Q1 hit 10% of total credit card balances, the highest rate since 2013, according to New York Fed data. But it remains far below the Financial Crisis peak of nearly 14%:

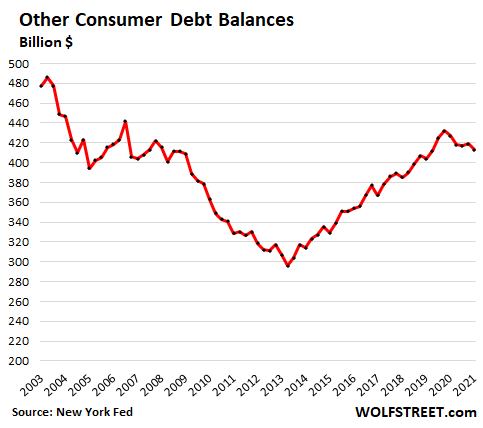

“Other” consumer debt balances also declined.

The balances of personal loans, lines of credit, and other loans from banks, shadow banks, peer-to-peer lenders, and payday lenders have declined during the Pandemic, after rising for years. This too was an effect of the stimmies and other measures. In Q1, balances dropped by $6 billion from the prior quarter and by $19 billion since Q4 2019, to $413 billion:

Serious delinquencies of 90+ days past due ticked up to 7.7% of total balances, having risen steadily since the recent low of 2017, but remain below the…

Read More: State of the American Debt Slaves: Fed “Confounded” as They Pay Down Credit