Why independent mortgage banks might want to sell themselves now

The Northeast is enjoying an old fashion Spring: cold and in some cases freezing even as May fast approaches. But the temperature in the housing sector is rising fast, belying the servile view within the Federal Open Market Committee that any inflation will be temporary.

The median price for existing home sales rose to $329,100 in March, a new high according to the National Association of Realtors. Prices soared 17.2% last month from a year earlier, marking the biggest price increase in NAR data going back to 1999. Bidding wars for homes located in hot markets are now considered normal.

Home prices are not the only part of the housing industrial complex that are on fire in terms of price inflation. The mortgage industry is in the midst of a post-boom consolidation, with several significant acquisitions and sales.

The purchase of Apollo portfolio company AmeriHome by Western Alliance Bancshares started the year, a good transaction for both sides priced around book value for the $850 million in mortgage servicing rights on the $95 billion loan book. Call it about 88 bp fair value of the servicing.

“AmeriHome’s successful results and unique business model proved to be highly attractive for Western Alliance Bank, which has a history of growing by adding specialized financing groups that excel through differentiated B2B expertise and strong client service,” said AmeriHome CEO Jim Furash.

Next, we saw the acquisition of Caliber Home Loans by New Residential, a large real estate investment trust that is externally managed by Fortress, a subsidiary of Softbank of Japan. Caliber had been owned by Loan Star Funds.

New Residential acquired Shellpoint in 2018 to bolster its lending business and allow it to own Ginnie Mae servicing assets. But the continued onslaught of mortgage prepayments compelled New Residential to acquire more lending capacity along with a significant MSR.

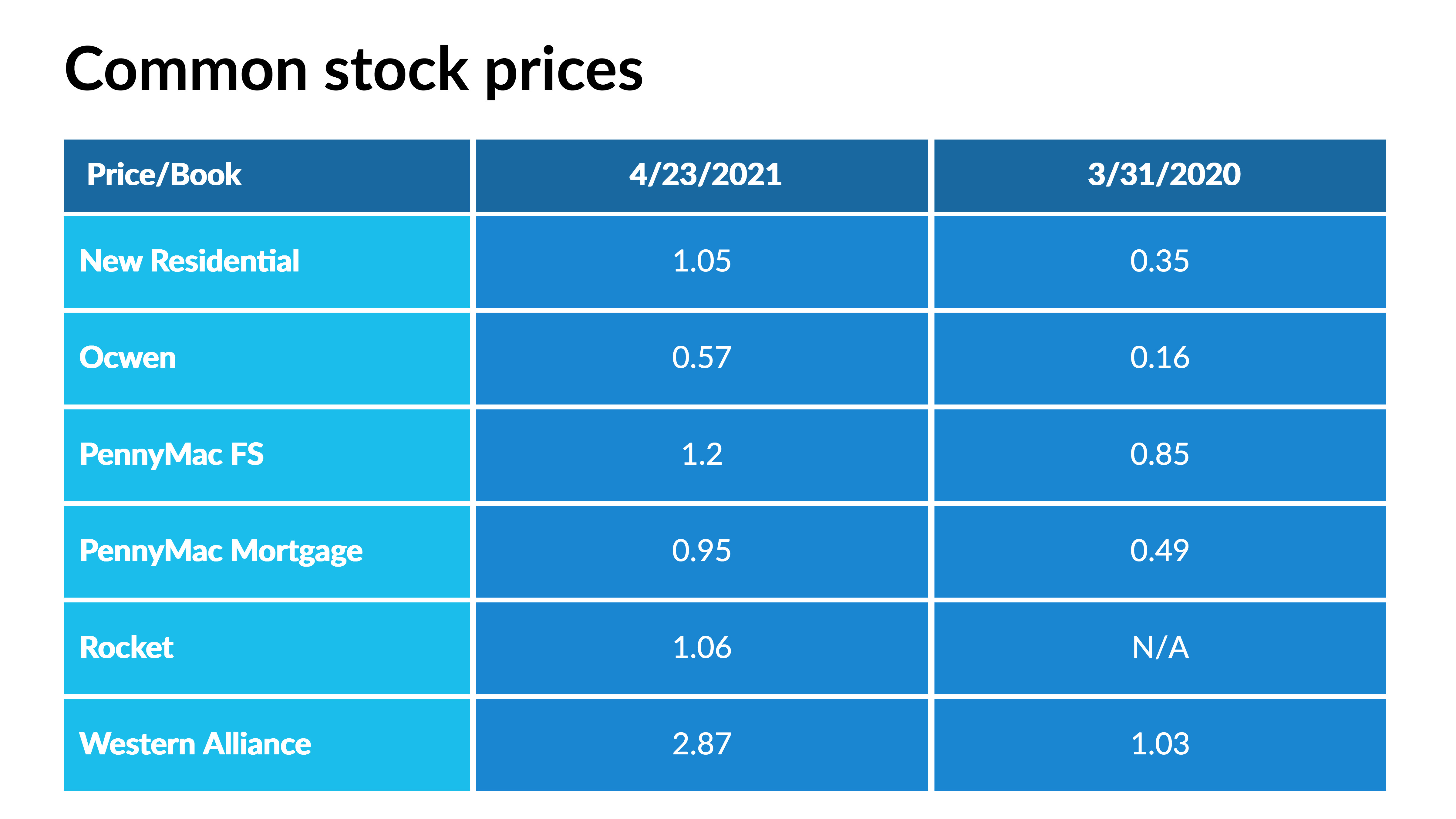

Led by former Citibank executive Sanjiv Das, Caliber is first and foremost known as a high touch lender focused on purchase mortgages. Like the Amerihome transaction, the deal was priced near book value. The table below shows the multiple of book value for the common stock of some of the mortgage firms mentioned in this article.

“We are excited to be joining the New Residential family,” said Das. “Our combination of strategies will allow us to accelerate our leading position in purchase lending, grow our digital direct to consumer and broker initiatives, and further propel our retail franchise.”

Combined, the two lenders Shellpoint (now NewRez) and Caliber will be a significant lender and also a large, taxable appendage of the REIT. New Residential CEO Michael Nierenberg, a former Bear Stearns banker like this writer, has gradually accumulated significant internal operating capabilities within New Residential. REITs are meant to be investors in non-operating assets in order to maintain passthrough status with the IRS, thus there may be another shoe to drop in this story.

The acquisition of Caliber begs the question as to when a spin-off of the entire New Residential lender/servicer will occur. In the case of Penny Mac, for example, the REIT, PennyMac Mortgage Investment Trust and the seller/servicer, PennyMac Financial Services, are legally separate entities. Both mortgage groups are bound together, however, by strong contractual and business ties, making the PennyMac binary, like New Residential and Fortress, arguably one entity in terms of risk and credit.

Another significant transaction came last week when Ocwen Financial announced the acquisition of a bulk MSR and the correspondent lending business of Texas Capital Bank. Ocwen will acquire MSRs related to $14 billion in unpaid principal balance of loans.

Ocwen previously had announced a strategic investment by Oaktree Capital Management for a $250 debt investment in the company, in part to fund purchases of MSRs.

In yet another deal, TIAA Bank announced the sale of its retail sales, operations and…

Read More: Why independent mortgage banks might want to sell themselves now