Financial Marketers Have a Big Opportunity to Snag Frustrated Consumers

One thing any marketer hates to do is miss a big opportunity to move the needle in a meaningful way instead of the usual incremental gains. Only one thing’s worse: Missing the opportunity and getting clobbered at the same time.

The current retail banking marketplace could be experiencing such a moment. Consumer intent — and actions — to change primary financial institution or to move more of their deposits and financial business to other providers, traditional or otherwise, appears to be rising sharply.

A confluence of evidence suggesting a significant opportunity/threat is unfolding. While not every data source supports this expectation equally — that hardly ever happens — the stakes loom too large to await total confirmation.

Before the pandemic, “switching intent” — meaning people who say they are definitely changing primary banks in the next six months — had been steady at about 9% of households and 14% of businesses for several years, according to Bruce Paul, Managing Director, Banking Research for Rivel. When the pandemic hit, switching intent fell sharply because of shuttered branches and uncertainty, but has since “come roaring back,” Paul tells The Financial Brand.

In Rivel’s latest wave of consumer interviews (104,000 people from November 2020 through January 2021) switching intent shot up to 17% among households and 31% among businesses, almost double the normal levels.

“I have never seen such a dramatic increase in switching behavior in the three decades I have been tracking this,” Paul states. “Even the figures during the financial crisis pale in comparison.”

Big Moment:

For banks and credit unions, there may never be as big an opportunity to quickly capture market share — or lose it.

As always, there is a difference between “intent” and actually doing something. Paul acknowledges this, but points to two additional statistics from their latest research:

- 31% of consumers are unhappy with their current banking provider.

- 15% are saying they’re actually going to switch in the next six months.

Both numbers are historically high, Paul observes. Pre-pandemic the “unhappy” figure would hover around the mid 20%s, while “actually planning to switch” was usually under 10%.

( Read More: Does Being a ‘Primary Financial Institution’ Mean What It Used To? )

Other Evidence that Consumers Are on the Move

Consumer intelligence company Resonate, which uses interviews plus artificial intelligence modeling to measure consumer banking behavior, finds a similar percentage of consumers with intent to switch banking providers: 16.4% of all U.S. adults (18 or older) as of April 2021. That equates to 36.7 million people, according to Ericka McCoy, Resonate’s CMO.

The company reports that 9.3 million people (roughly 4% of all U.S. adults) say they are actively switching, a much lower figure than what Rivel reports. The companies use different research methodologies, however, so a direct comparison is not possible. Resonate does say that about a third of active switchers (3.3 million people) are planning to change financial institutions by July 2021.

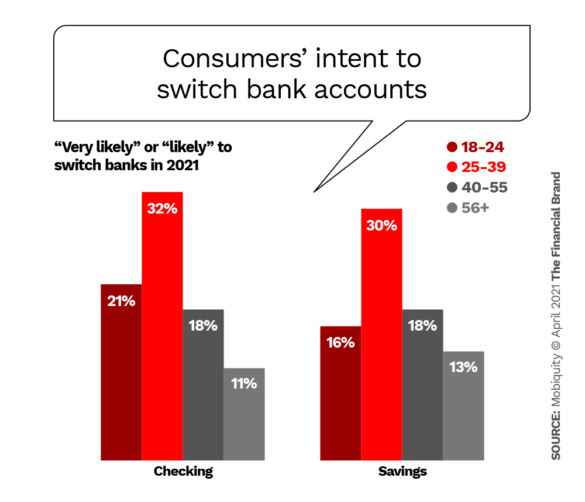

Digital consultancy Mobiquity surveyed about 2,445 U.S. adult consumers in January 2021 and found that 11% of the respondents said they had already made an account switch for either a checking or savings account in the past year. The company also asked respondents to predict their switching behavior in 2021.

In both instances — those who had switched accounts and those who were expected to do so —Millennials were the dominant group.

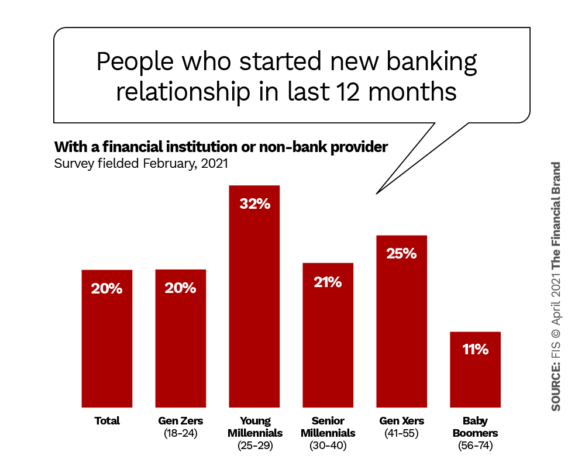

In its latest PACE research, FIS found that one fifth of 1,015 U.S. consumers surveyed in early February 2021 said they had started a new banking relationship in the previous 12 month period.

All this evidence doesn’t necessarily mean that consumers are moving their primary banking relationship….

Read More: Financial Marketers Have a Big Opportunity to Snag Frustrated Consumers