To trust or not to trust: Mumbai ITAT confirms exclusion of offshore trust’s

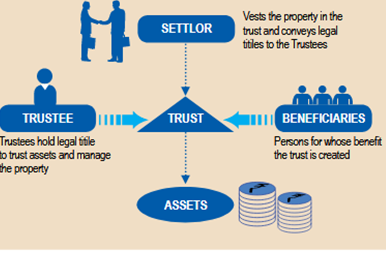

Private trusts are a popular tool among rich families with respect to succession planning. Trusts are a legal arrangement whereby assets are placed in the care of an individual who manages them for the benefit of someone else (Figure 1). Trusts can be further classified as specific or discretionary based on the scheme of distribution.

However, it appears that offshore trust structures are increasingly being used as a means of money laundering rather than lawful tax planning. Consequently, the Income Tax Department has unveiled various private offshore trusts and imposed tax liability on the beneficiary owners. This has led to an increase in reassessment proceedings and dissatisfaction among residents who claim that they have been subjected to wrongful tax liability.

In a recent case, the Mumbai Income Tax Appellate Tribunal (ITAT) provided relief to one individual, holding that offshore trusts are an acceptable form of tax planning and that a beneficiary of an offshore discretionary trust cannot be taxed on the entire corpus fund merely because they have been given the power to appoint or reappoint trustees.

Figure 1(1)

A search and seizure operation was conducted on Mr Yashovardhan Birla (the assessee) under Section 132 of the Income Tax Act 1961 for assessment years 2008-2009 to 2013-2014. On the discovery of undisclosed gold and diamond jewellery, a notice was served on the assessee under Section 16 of the Wealth Tax 1957. Pursuant to the notice, on 25 March 2015 the assessee filed his return on wealth for assessment year 2008-2009, declaring his net wealth to be Rs2,30,03,500 (almost six times the amount declared in the original return of wealth).

In addition, based on information received from the Foreign Tax and Tax Research division of the Central Board of Direct Taxes, it was discovered that the assessee was a beneficiary of more than 70 offshore bank accounts and immovable properties held by offshore entities. These offshore entities held these assets under an offshore discretionary trust, which had been created by the late Pratap Malpani in 1989 and was executed by an offshore trustee, Albany Trustee Company Limited. The list of beneficiaries included:

- the settlor;

- the settlor’s wife, sons, daughters in law and lineal descendants;

- Ashokvardhan Birla (the settlor’s brother in law) and his wife, Sunanda Birla (the settlor’s sister), children (who included the assessee), children in law and lineal descendants; and

- charitable organisations in India and Guernsey.

The assessment officer labelled the amount held in these offshore bank accounts as being on par with cash in hand and classified them as unproductive assets under Section 2(ea) of the Wealth Tax Act. The assessment officer included a sum of Rs96,29,53,356/- in the assessee’s net wealth.

The assessee filed an appeal against the assessment officer’s order with the commissioner of income tax, but it was dismissed. As such, the assessee filed an appeal with the Mumbai ITAT.

The questions before the Mumbai ITAT were as follows:

- Was having a beneficial interest in offshore bank accounts held by offshore entities tantamount to being the ultimate beneficiary owner, resulting in the amount being included in the assessee’s net wealth and the assessee being taxed accordingly?

- Was having the power to appoint or reappoint trustees the same as having control over the trust and the trust losing its independent identity? Further, could the entire corpus fund of the offshore discretionary trust with offshore trustees be included in the assessee’s net wealth and net income when the assessee had never been allotted any share in the income or received any income from the trust?

The Mumbai ITAT rendered a comprehensive and detailed decision on the nature of the trust and the recitals of the trust deed. It noted that Malpani had created the trust for the benefit of several beneficiaries, including the assessee and charitable…

Read More: To trust or not to trust: Mumbai ITAT confirms exclusion of offshore trust’s